")

This comprehensive guide provides an in-depth analysis of Income Tax Return Filing for Individuals and HUFs, specifically focusing on the ITR-2 Form. If you are navigating the complexities of capital gains, foreign assets, or multiple properties, this resource outlines the technical requirements and compliance standards necessary for a successful submission.

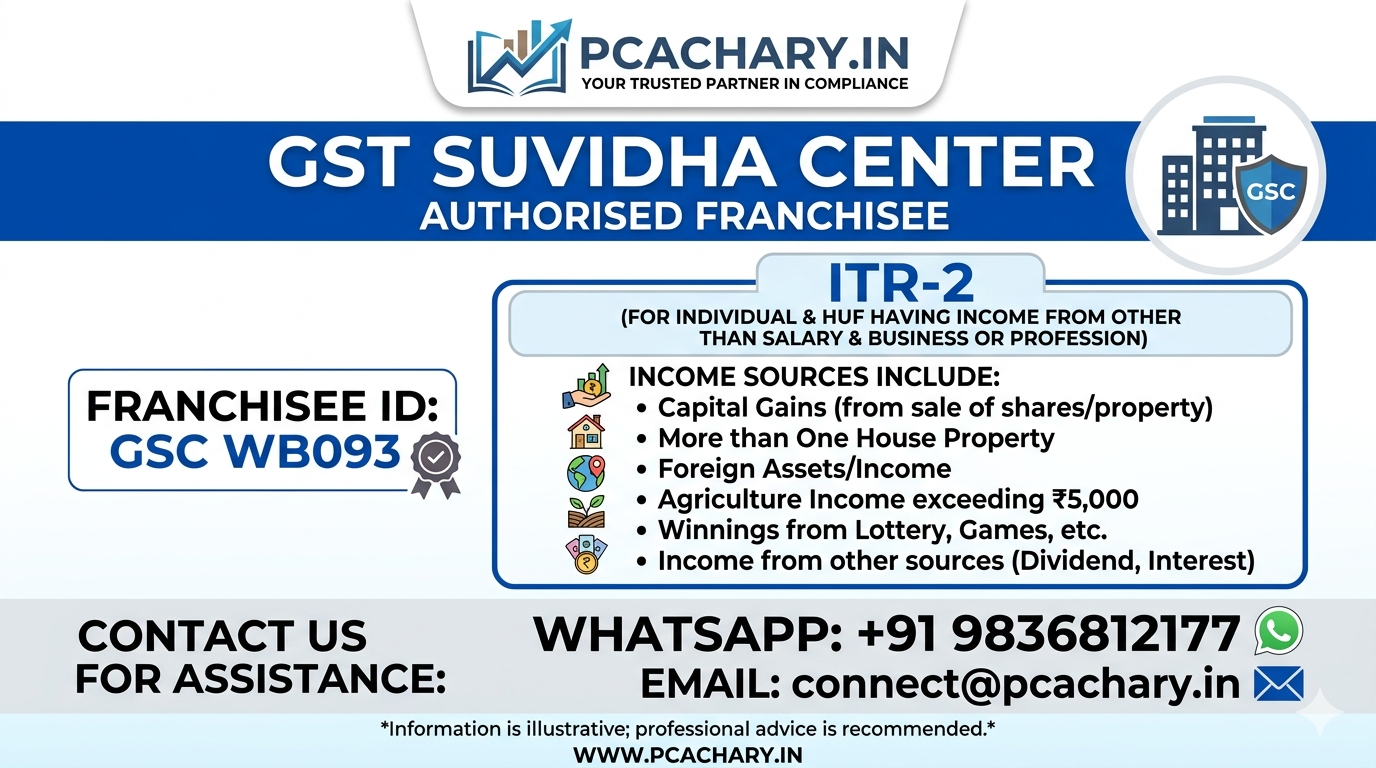

For personalized assistance and professional filing services, you can connect with the GST Suvidha Center (Franchisee ID: GSC WB093). Expert support is available via the official website at Pcachary.in, through email at connect@pcachary.in, or via WhatsApp at +91 9836812177.

Understanding the ITR-2 Landscape

The Indian taxation system is structured to categorize taxpayers based on the nature and volume of their income. While ITR-1 (Sahaj) is the most common form for salaried individuals with simple financial profiles, the ITR-2 is a more robust and detailed document. It is designed for individuals and Hindu Undivided Families (HUFs) who do not have income from “Profits and Gains of Business or Profession” but possess financial complexities that exceed the limitations of simpler forms.

Who Must File ITR-2?

ITR-2 is applicable to individuals or HUFs who fall into the following categories:

- Exceeding the Income Threshold: Individuals with a total income exceeding ₹50 lakh.

- Multiple House Properties: If you own and earn income from more than one house property.

- Capital Gains: Any income derived from the sale of assets such as real estate, shares, mutual funds, or gold.

- Foreign Assets and Income: Residents who own assets outside India (such as foreign bank accounts or stock options in foreign companies) or earn income from foreign sources.

- Director Status: Any individual who held a directorship in a company at any time during the financial year.

- Unlisted Equity Shares: Investors who held unlisted equity shares at any time during the year.

- Agricultural Income: If the agricultural income exceeds ₹5,000.

- Residential Status: Individuals classified as “Not Ordinarily Resident” (RNOR) or “Non-Resident” (NR).

Who Cannot File ITR-2?

It is critical to note that ITR-2 is strictly prohibited for any individual or HUF whose income includes earnings from a business or a profession. This includes freelancers, consultants, or sole proprietors who operate under a business structure. For those individuals, ITR-3 or ITR-4 would be the appropriate filing avenues.

Technical Components of ITR-2 Filing

Filing ITR-2 requires a meticulous breakdown of various income schedules. Unlike simpler forms, ITR-2 demands detailed disclosures regarding investments and asset movements.

1. Income from Salary

Even though ITR-2 is used for complex profiles, many filers are still salaried employees. The form requires details from Form 16, including gross salary, perquisites, and profits in lieu of salary. It also accounts for exempt allowances such as House Rent Allowance (HRA) and Leave Travel Allowance (LTA).

2. Income from House Property

If you own multiple properties, ITR-2 requires the address, ownership percentage, and the “Annual Lettable Value.” You can claim a standard deduction of 30% for repairs and maintenance, as well as deductions for interest paid on home loans (u/s 24).

3. Capital Gains (Schedule CG)

This is often the primary reason taxpayers shift to ITR-2. You must categorize gains into:

- Short-Term Capital Gains (STCG): Assets held for shorter durations (e.g., equity shares held for less than 12 months).

- Long-Term Capital Gains (LTCG): Assets held for longer durations (e.g., real estate held for more than 24 months).

- Grandfathering Provisions: Specifically for equity investments made before January 31, 2018, the “Cost of Acquisition” calculation follows specific Fair Market Value (FMV) rules.

4. Income from Other Sources (Schedule OS)

This includes interest from savings accounts, fixed deposits, dividends, and any family pension. ITR-2 now requires a quarterly breakup of dividend income to accurately calculate interest under section 234C for defaults in payment of advance tax.

Deductions and Tax Benefits

The Indian Tax Code allows several deductions to reduce the taxable burden, primarily under Chapter VI-A.

- Section 80C: The most popular section, allowing deductions up to ₹1.5 lakh for investments in PPF, ELSS, LIC, and EPF.

- Section 80D: Deductions for health insurance premiums for self, family, and parents.

- Section 80TTA/80TTB: Interest income deductions for individuals and senior citizens.

- Section 80G: Deductions for donations made to charitable organizations or relief funds.

The Role of GST Suvidha Centers in Income Tax Compliance

Navigating the schedules of ITR-2—especially Schedule FA (Foreign Assets) or Schedule AL (Assets and Liabilities)—can be daunting. Errors in reporting foreign income or miscalculating capital gains can lead to notices from the Income Tax Department.

The GST Suvidha Center (Franchisee ID: GSC WB093) serves as a professional bridge, ensuring that your financial data is translated accurately into the tax return. By utilizing professional services, taxpayers minimize the risk of:

- Incorrect tax credit (TDS) claims.

- Under-reporting of income.

- Missing deadlines that lead to penalties under section 234F.

For expert guidance on your ITR-2 filing, visit Pcachary.in. You can also reach out for a consultation via WhatsApp at +91 9836812177 or email connect@pcachary.in.

Step-by-Step Filing Process for ITR-2

Stage 1: Documentation Gathering

Before beginning the online process, ensure you have the following:

- PAN and Aadhaar Card.

- Form 26AS & AIS/TIS: To verify TDS and significant financial transactions.

- Capital Gains Statements: From your stockbroker or mutual fund house.

- Bank Statements: For all active accounts held during the financial year.

- Foreign Income Proof: If applicable.

Stage 2: Validation of Data

The Annual Information Statement (AIS) is a crucial tool provided by the department. It tracks almost every financial footprint you leave. When filing ITR-2, every entry in the AIS must be reconciled. If the AIS shows a share sale that you haven’t recorded, it will trigger a discrepancy flag.

Stage 3: Filling the Schedules

ITR-2 is composed of several “Schedules.” You must select only those relevant to you. For instance, if you don’t own foreign assets, you skip Schedule FA. However, if you are a director in a private limited company, you must provide the DIN (Director Identification Number) and the company’s PAN.

Stage 4: Verification (e-Verification)

A return is not considered “filed” until it is verified. The most efficient way is e-Verification using Aadhaar OTP. Alternatively, you can send a physical copy of the ITR-V to the Centralized Processing Center (CPC) in Bengaluru within the stipulated timeframe.

Common Pitfalls in ITR-2 Filing

- Ignoring Schedule AL: If your total income exceeds ₹50 lakh, you must disclose the value of your assets (movable and immovable) and liabilities. Failure to do so is a compliance breach.

- Incorrect Residential Status: Tax liability changes significantly based on whether you are an ROR, RNOR, or NR. Misidentifying this status is a common error for those living abroad for part of the year.

- Dividend Income Misreporting: Dividends are now taxable in the hands of the shareholder. Reporting these under the wrong head or failing to provide the quarterly breakup can result in unnecessary interest penalties.

- TDS Mismatch: Always ensure the TDS reflected in your Form 26AS matches the credit you claim in the return.

Why Choose Professional Assistance?

While the Income Tax Department has simplified the e-filing portal, the underlying tax laws remain complex. The GST Suvidha Center (GSC WB093) provides a comprehensive suite of services that goes beyond just data entry. We offer:

- Tax Planning: Identifying legitimate ways to save tax within the legal framework.

- Accuracy: Using specialized software to ensure all calculations, especially for LTCG with indexation, are precise.

- Peace of Mind: Professional handling reduces the likelihood of receiving scrutiny notices.

To engage our services for ITR-2 filing or other tax-related queries, please visit Pcachary.in. Our team is ready to assist you through WhatsApp at +91 9836812177 or via email at connect@pcachary.in.

Conclusion: Staying Compliant in a Digital Era

Income tax compliance in India has moved toward a “pre-filled” and “data-driven” model. The synergy between the GST portal and the Income Tax portal means that the government has more visibility into your financial health than ever before. For individuals and HUFs with diverse income streams, the ITR-2 is the most appropriate vehicle for transparent reporting.

Proper filing is not just about paying tax; it is about building a clean financial record that facilitates visa applications, loan approvals, and future investments. Ensure your filing is handled by authorized professionals who understand the nuances of the law.

Contact Information:

- Website: Pcachary.in

- Franchisee ID: GSC WB093

- WhatsApp: +91 9836812177

- Email: connect@pcachary.in

By choosing the right partner for your tax journey, you ensure that your financial future remains secure and compliant with the latest regulations of the Government of India.

")

")

Reviews

There are no reviews yet.